New Generation Of Derivatives: Tranched Value Securities

A guest post from Nikolay Zvezdin explains a new product model, the Tranched Value Security. Tranched Value Securities (TVS) are the next step in derivatives and structured products development. TVS allows

November 21, 2019 - Editor

Category: Fixed Income

A guest post from Nikolay Zvezdin explains a new product model, the Tranched Value Security.

- Tranched Value Securities (TVS) are the next step in derivatives and structured products development.

- TVS allows to securitize and tranch values of securities, rather than cash-flows or pooled asset-base.

- TVS transforms risk-free securities into speculative instruments, and vice versa.

- TVS empowers leveraging returns without leverage.

- Single stock or bond, or any other standalone security or derivative can be collaterized with TVS.

This is a guest post from Nikolay Zvezdin:

Most people are aware of derivatives and structured products that allow to hedge risks, leverage returns or transform performance of underlying. That’s an “old school” and established practice, which was quite successful, given that since 1998 global OTC derivatives market has grown from nearly $80 to over $500 trillion in 2017 (6x times greater than global GDP).

The most complex derivatives are typically structured products that result from securitization process. However, while most of the sources and textbooks define securitization as the process of pooling various assets or cash-flows with subsequent sale of the corresponding tranches to third party investors as independent securities, none of the existing instruments provide securitization of individual (standalone) assets or cash-flows. So, what that means? – Until recently, no one was able to securitize a single stock or bond and sell various tranches of it, which would generate different returns.

But times have changed, and with the recent developments, soon it might be possible. A possible candidate for this role is Tranched Value Security (patent pending).

Tranched Value Securities are first described in the paper published on SSRN: Tranched Value Securities. According to the paper:

Tranched Value Security (TVS) is a security whose income payments, and hence value is derived from and collateralized (or "backed") by the value of a single asset, group of assets, stream of cash-flows or any other entity or product possibly having a determinable value (and / or price). Value of TVS is derived either from a value share of a specific underlying, or from a minimum contract value, which can be a value share of a specific underlying at the contract initiation, given that a higher-level (or “prior”) TVSs are satisfied.

What does that imply? – It implies that now, two or more parties holding the same asset or cash-generating contract will be able to earn different rates of return, within the same underlying, whether it’s a financial asset or derivative, or real asset, during the same holding period, in the case if parties hold different value tranches. And that is the result of a single feature – value tranche seniority, where any TVS holder is able to exercise tranche only if the more senior one was satisfied. That means that if the underlying experienced a significant decline in value, exceeding detachment point of junior value tranche – it will default, while the senior TVS might still have positive value.

That is imposed by the following payment model:

where TVS_i_t is the value of Tranched Value Security (TVS_i), i.e. i-th value tranche at time t=n of underlying (S_t); S_t is the price of underlying at time t=n; w_i is the fixed weight of i-th value share corresponding to the specific underlying (S_t) at the contract initiation (t=0); X_i is the minimum corresponding value of TVS_i share at any time, which is set fixed and equals to w_i x S_t during the contract initiation at t=0; TVS_i-1_t is the value of higher-ranked Tranched Value Security (TVS_i), i.e. i-1-th value tranche at time t=n of underlying (S_t), which must be satisfied before any subsequent Tranched Value Security (TVS_i+1) can be fulfilled.

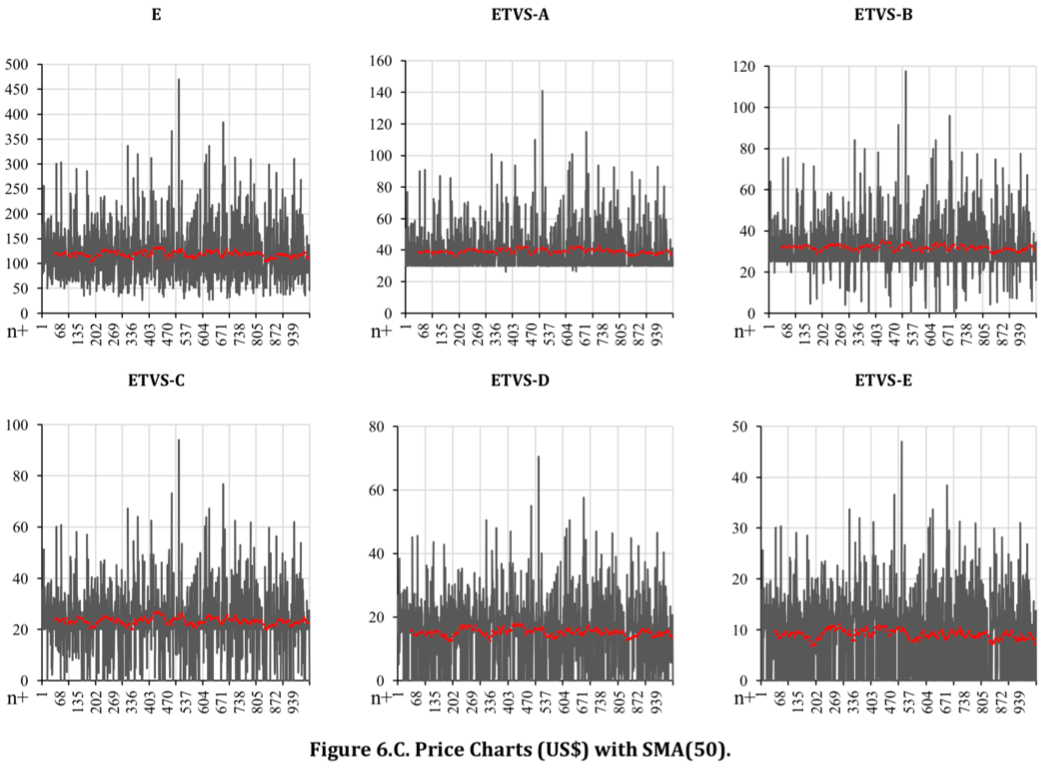

To illustrate the possible effects of this model, imagine that underlying equity (E) has a price of $100.0 and is used as collateral for five Tranched Value Securities. TVSs have 30% (ETVS-A), 25% (ETVS-B), 20% (ETVS-C), 15% (ETVS-D), 10% (ETVS-E) value share claims (where all value share claims sum up to 100% of the underlying), and set fixed to equal $30.0, $25.0, $20.0, $15.0, and $10.0 minimum value claims (where all minimum value share claims sum up to $100.0 of E) if the higher value share is satisfied. In such issuance conditions, ETVS-A has 30% value share claim of underlying, or $30.0 minimum value share, ETVS-B has 25% value share claim of underlying, or $25.0 minimum value share if more senior TVS (ETVS-A) is satisfied, and so on.

Based on lognormal distribution modeling of underlying price, that has expected annual return of 10%, and standard deviation of 50%, simulation for 1,000 periods produces the following results:

- All securities experience various price fluctuations, with ETVS-A being the most stable, while ETVS-E and ETVS-D being the most volatile.

- ETVS-E and ETVS-D experienced defaults the most often in 37%, and 22% cases respectively out of 1,000 simulated periods.

- Default rates are compensated by the highest maximum returns of the three most junior value tranches (ETVS-C, ETVS-D, ETVS-E). This is the result of junior value tranches losing all value (having a market price of zero), when the value of ETVS-A becomes equal to the value of underlying equity security, due to its value seniority.

- ETVS-A and ETVS-B almost always have a fixed price floor below which their value barely falls, unless the underlying equity security experiences severe price declines.

- Return correlations depict that between some security pairs there is almost no co-movement at all (correlation of nearly 0.1 between ETVS-D and all other securities, correlations of 0.13-0.23 between ETVS-C and all others), while returns of the most senior tranches are the most consistent with the returns of underlying equity security.

- Based on the statistical assessment, ETVS-D generated the highest mean return, with the value of 244%, while the mean return of the underlying equity security was 24% (10.0x less than the return of ETVS-D). The lowest mean return of -10% was generated by ETVS-E due to the significant number of defaults.

- Range of returns is the highest for ETVS-D, and ETVS-C, while for ETVS-A it is lower than even for the underlying, as this value tranche essentially contains less risk than the underlying equity security, which is evident from the twice reduced standard deviation.

The results depict a significant performance transformation of the original underlying due to tranching of its value. Not only the return distribution parameters changed, but also the shapes of distributions were significantly modified due to securitization of values with the risk-return profiles of securities. This suggest that TVS holders obtain major diversification benefits in crisis and positive market situations, while the securities might satisfy various risk appetites of potential investors.

More details of the potential securities issuance with other underlyings as case studies can be found in the original manuscript, which produce consistent results displaying significant performance transformations.

While the example shown concerns simulated equity securities, applications of TVS are significantly wider than that. TVS could potentially be issued on any asset, liability, equity, interest rate, exchange rate, market index, notional value or any other instrument, which has an assessible market value or price. TVSs can be issued with the varying initial issuance parameters, such as the weight of the value TVS can claim in the underlying. While the higher value share would represent less risk for the potential security buyers, and a smaller value share could significantly improve returns although amplifying the corresponding risks, which all together affect attachment and detachment points in TVS. Furthermore, the minimum value share claim can equal to minimum value claim, or it can be two different values, and instead of being fixed, can be floating.

Moreover, TVS can have maturity dates, changing equity securities in some cases to fixed-income instruments. The opposite can be done with TVSs with debt as underlying by rolling the TVS issuance in new debt with the same characteristics as the original one, thus transforming the initial bond into fixed-income equity or perpetual fixed income. Another possible modification of TVS is the issuance with separate groups of underlying.

For example, one issue of TVS could have the bond’s face value as underlying, while another TVS issue could have bond’s coupons as underlying. Same applies to equity and corresponding dividends, which would enhance performance of some value tranches on the expense of others. Also, TVS could be issued with option, forward or swap-like terms, whereas one type forces execution of value tranche on a specified future date, another one gives a right to execute the contract on or before the specified maturity, and swap forcing the exchange of differences in periodic values instead of the notional value exchange. Tranched Value Securities can be further be modified and issued on existing TVSs (TVS-Squared), making them similar to Credit Default Swaps Squared, where a particular value tranche is backed by a number of specific value tranches in other TVSs.

Additional mechanisms could be implemented similar to credit enhancements. Thus, by varying internal and external parameters of Tranched Value Securities, the possibilities for creating new types of instruments are endless, which could potentially satisfy a wide range of market participants with different objectives – be it speculation, long-term investment, hedging operations or any others, which together with coordinated work of market participants, could improve market efficiency and asset price revelation.

Popular

Most Viewed

Articles

Sep. 15, 2022

Tradefeedr Hires Alexis Fauth as Head of Data Science and Client Analytics

Sep. 06, 2022

Siege FX announces the launch of NetFix

Aug. 02, 2022

OSTTRA and LCH collaborate to reconcile bilateral OTC trade data

Jul. 26, 2022

Sell-side systems in need of upgrade for new risk reality

Jul. 15, 2022